How to Buy HDB in Singapore: Your Complete 2026 Step-by-Step Guide

Buying your first HDB flat involves more moving parts than most buyers expect. This guide walks you through every stage — from checking eligibility to collecting your keys — with the mortgage and CPF checkpoints clearly flagged.

What You Need Before You Start

Before you look at a single flat, three financial questions need answers:

Running these three checks first — before falling in love with a flat — saves considerable time and prevents the disappointment of a rejected loan application. Use the Nexus Advanced Calculator to get a real-time read on all three. For a deeper understanding of TDSR and MSR, read our guide: TDSR vs MSR Explained.

The Journey: Stage by Stage

The HDB purchase journey has five main stages. Mortgage decisions happen at Stage 1 and Stage 3 — earlier than most first-time buyers expect.

Get Your HFE Letter Mortgage CPF

The HDB Flat Eligibility (HFE) Letter is your starting point for both BTO and resale purchases. Apply via the HDB Flat Portal. It confirms your eligibility, the CPF housing grants you qualify for, and — if you intend to use an HDB loan — the maximum loan amount HDB will offer. The HFE Letter is valid for 9 months. Do not skip this step: you cannot book a flat or submit a resale application without one.

Decide: BTO or Resale?

A BTO flat is purchased from HDB at a subsidised price with a ballot. Waiting time is typically 3–5 years from ballot to keys. A resale flat is an existing flat on the open market — you can move in within 2–3 months of completing the transaction. BTO is generally cheaper; resale gives you choice of location, size, and immediate occupation. Your choice here determines your timeline for everything that follows.

Secure Your Mortgage Critical

This is where the most consequential financial decision in your purchase is made: HDB loan or bank loan? If you qualify for both, the comparison involves your cash reserves, income level, appetite for rate management, and long-term plans. For a bank loan, obtain an In-Principle Approval (IPA) from your chosen lender — it is free, non-binding, and valid for 30 days. A mortgage broker can obtain IPAs from multiple banks simultaneously.

Reserve the Flat & Exercise the OTP

For resale: negotiate with the seller, pay a booking fee (Option Fee) of up to S$1,000 to receive the Option to Purchase (OTP). You have 21 calendar days to exercise the OTP by paying the Option Exercise Fee. Total deposit at exercise is 5–10% of the purchase price, which forms part of your down payment. For BTO: HDB issues you a flat selection appointment after a successful ballot. You pay the downpayment directly to HDB upon flat selection.

Complete the Purchase & Collect Keys CPF

HDB schedules a completion appointment — typically 8–12 weeks after OTP exercise for resale. At this appointment you sign the mortgage, execute the CPF charge, pay the remaining balance of your down payment, and collect the keys. Your bank loan disburses on the same day. If using an HDB loan, the disbursement is coordinated by HDB directly.

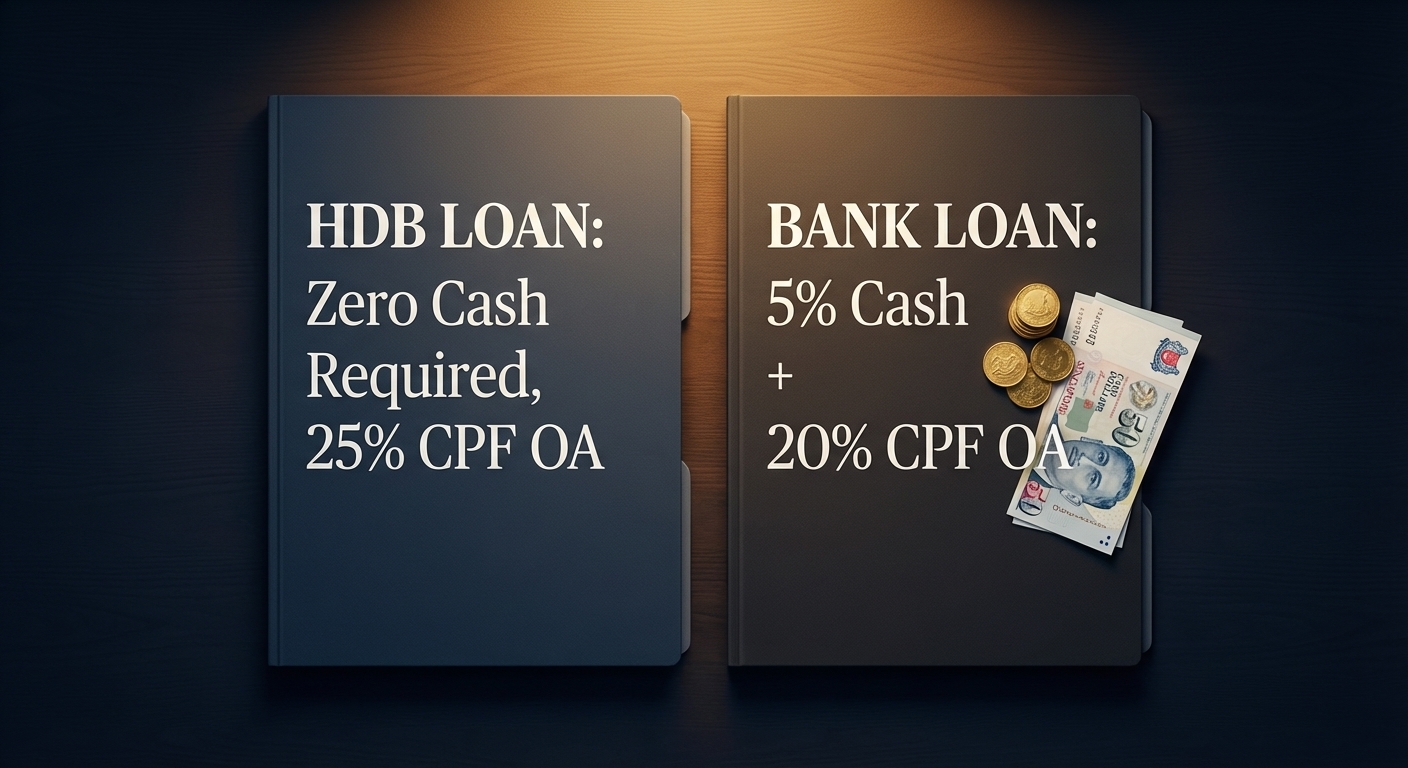

The Down Payment: Where Your Money Comes From

HDB loan: full 25% from CPF OA, zero cash required. Bank loan: minimum 5% cash, 20% from CPF OA. On a S$900,000 flat, that is S$45,000 cash minimum for a bank loan versus zero for HDB loan.

On a S$900,000 flat, the down payment split looks like this:

HDB Loan: S$225,000 total (25%) — the entire amount can come from your CPF OA. Zero cash required. This is the most significant practical advantage the HDB loan offers first-time buyers with limited liquid savings.

Bank Loan: S$225,000 total (25%) — a minimum of S$45,000 (5%) must be in cash. The remaining S$180,000 may come from CPF OA. Cash grants received from HDB can offset this requirement in some cases.

For a full breakdown of how the MAS stress test shapes your maximum loan amount, and how TDSR and MSR interact with your total borrowing capacity, work through both linked articles before committing.

Your Mortgage Broker

Talk to Dan Ler — Nexus Mortgage SG

I personally check your TDSR, MSR, and CPF position, compare every available HDB and bank loan package, and guide you through each stage of your purchase — free of charge. The bank pays my fee, not you.

WhatsApp Dan Now — Free Consultation →Prefer to run the numbers first? Use the free Advanced Mortgage Calculator with 2026 TDSR/MSR stress-test logic.

Nexus Mortgage SG is an independent mortgage advisory in Singapore. This article is for general informational purposes only and does not constitute financial or legal advice. HDB eligibility criteria, grant amounts, and bank lending guidelines are subject to change. Figures are illustrative and based on conditions as of April 2026. For official HDB purchase information, visit HDB: Buying a Flat. For mortgage loan options, see our full comparison: HDB vs Bank Loans.