New Launch Condo Financing in Singapore (2026): Progressive Payment, IPA, and TOP Strategy

A new launch condo in Singapore is a S$1.5M to S$5M+ commitment. You get a three-week S&P clock, a multi-year construction tail, and a SORA-linked partial-drawdown loan that behaves nothing like a resale mortgage. Three things shape the next 25 years of cashflow: the IPA, the loan tier, and how well your lock-in lines up with TOP. Here is how Building Under Construction (BUC) financing actually works in 2026, and where buyers lose money they didn’t need to.

- Progressive Payment Scheme: how the stage payments work

- Progressive payment calculator

- PPS vs Deferred Payment: why DPS is no longer offered for residential

- The OTP clock and why an IPA is non-negotiable

- TDSR, MSR, and the loan-tier rate game

- SORA spreads on a partially-drawn BUC loan

- TOP, lock-in, and the refinance window

- Five expensive new-launch mistakes

- How a broker structures the deal

- Common questions

Progressive Payment Scheme: How the Stage Payments Work

Singapore residential BUC projects sell on the Progressive Payment Scheme (PPS). You pay the developer in instalments tied to construction milestones, and the bank disburses your loan in matching tranches. Interest is charged only on what has already been drawn, so your monthly instalment starts small and climbs as the project goes up.

PPS pays the developer in tranches synced to the building’s construction milestones. The bank’s draw schedule mirrors this, so your interest cost climbs over time instead of starting at the full quantum on day one.

| Stage | % of Purchase Price | What Triggers It |

|---|---|---|

| Booking Fee | 5% | OTP signed at the developer’s sales gallery (cash + CPF) |

| Sale & Purchase Agreement | 15% | S&P exercised, bringing you to 20% by ~8 weeks of OTP |

| Foundation | 10% | Foundation works completed |

| Reinforced Concrete Framework | 10% | Structural framework completed |

| Brick Walls | 5% | Partition / brick walls completed |

| Ceiling & Roofing | 5% | Ceilings and roofing completed |

| Doors, Windows, Wiring & Plastering | 5% | Door and window frames, electrical wiring, internal plastering |

| Car Park, Roads & Drains | 5% | Car parks, roads and drains completed |

| TOP | 25% | Temporary Occupation Permit issued — you collect keys |

| CSC | 15% | Certificate of Statutory Completion issued |

You pay the first 5% in cash and CPF at booking. The remaining 95% is your loan, cash and CPF mix, drawn against the milestones above. Your monthly interest grows as the drawdowns accumulate, not from day one.

Progressive Payment Calculator

Enter the price, your loan size and rate. It shows how much of your loan is drawn at each construction milestone, and how the monthly instalment ramps up as the building goes up.

| Construction milestone | Loan drawn | Est. monthly |

|---|

Estimate only. Assumes your 25% downpayment funds the first stages and the loan draws from there; instalments shown are principal + interest on the amount drawn so far, over your full tenure. During construction some banks charge interest-only on drawn amounts — ask your banker. Use the all-in floating rate (SORA + spread).

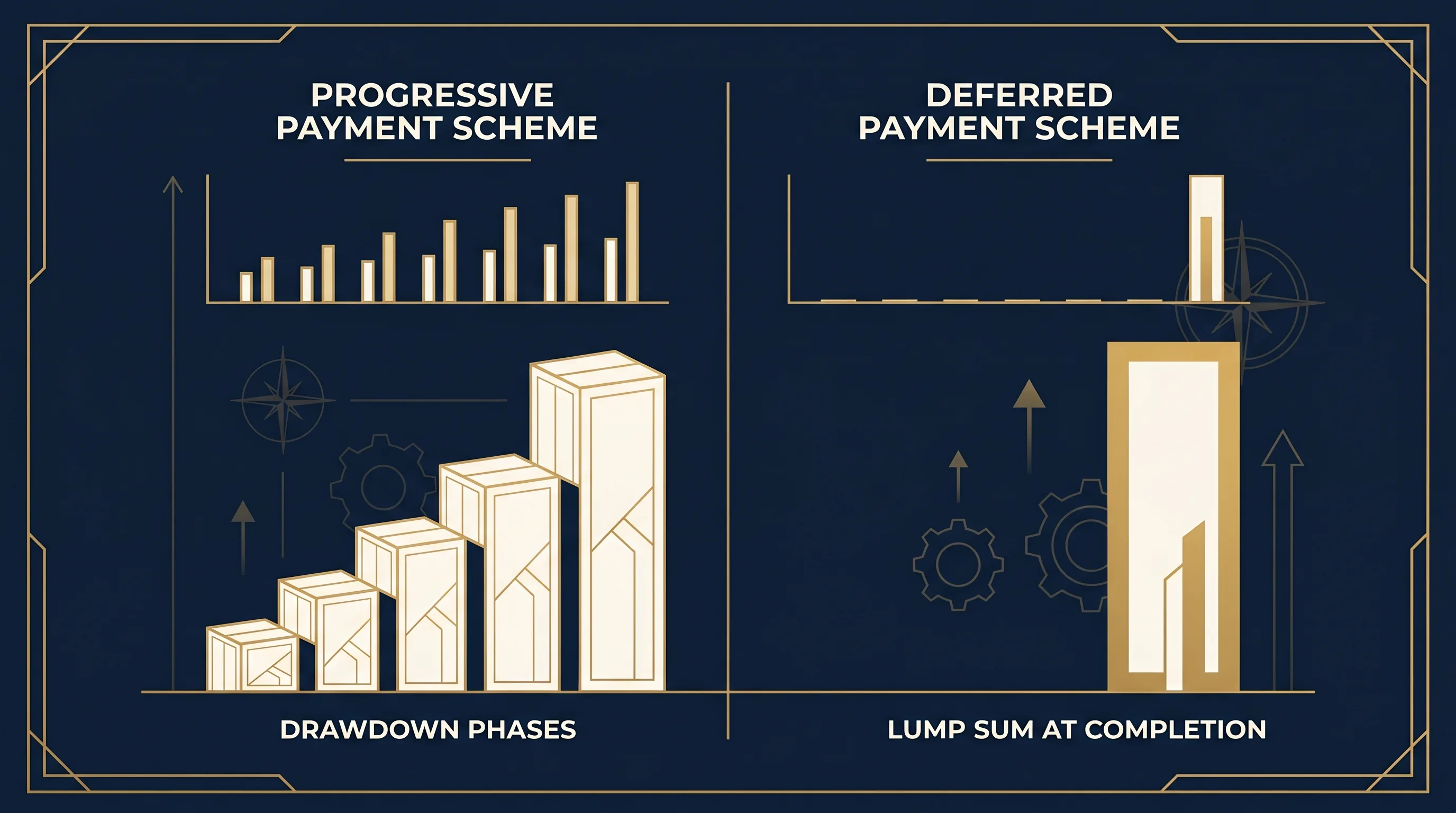

PPS vs Deferred Payment: Why DPS Is Off the Table for Residential

The Deferred Payment Scheme (DPS) let buyers pay 10–20% upfront and defer the rest until TOP. It was withdrawn for residential in 2007 to cool speculation. For new launches in 2026, residential PPS is the default. DPS-style structures only turn up on commercial deals and a bit of EC tail-end inventory.

PPS spreads loan disbursement across construction milestones, while DPS concentrates it at TOP. Cashflow timing, interest accrual, and the TDSR check all differ.

For most private property buyers the question is moot. A new launch in 2026 means PPS. The real decisions are which lender to anchor with, the SORA spread tier, and how to time your lock-in expiry against TOP.

The OTP Clock and Why an IPA Is Non-Negotiable

A new launch OTP commits a 5% booking fee. That is S$100K on a S$2M unit, or S$250K on a S$5M unit. You then have roughly three weeks from OTP to exercise the S&P and pay the next 15%. Miss the window and the booking fee is gone.

An In-Principle Approval is the bank’s written commitment to lend a specific quantum at a specific tenure, subject to valuation. It checks your income, your debt servicing under TDSR 55% (and MSR 30% if you’re buying an EC), and the MAS 4% stress test, all before any cash hits the developer’s account. Without one, your booking fee is riding on guesswork.

The booking fee is committed at the showflat. The IPA should already be in hand.

New launch IPAs are fragile for a specific reason. Valuations lean on developer pricing rather than transacted comparables. If the unit prices above a bank’s PSF ceiling, the loan quantum drops and you cover the gap in cash. A single-bank IPA that “looks fine” can still fail at another bank’s valuation desk on the very same unit.

“Run parallel IPAs across three to five lenders before you sign the OTP. New launches value very differently from bank to bank. One lender’s S$1.5M ceiling can be another’s S$1.65M, and that S$150K gap decides whether you exercise or forfeit.”

TDSR, MSR, and the Loan-Tier Rate Game

Every new launch loan goes through the same MAS framework:

- Your total monthly debt servicing under TDSR 55% (mortgage plus car, cards and personal loans) cannot exceed 55% of gross income.

- If you’re buying an EC, MSR caps the mortgage instalment at 30% of gross income. Private condos and landed are not subject to MSR.

- The 4% stress test recalculates TDSR and MSR against a 4.0% p.a. floor, not the live SORA rate. Qualifying at today’s rate doesn’t mean you pass the test.

- LTV is 75% on your first housing loan, dropping to 45% on a second.

Here is what most new launch buyers miss. Banks tier their pricing by loan quantum. Same unit, same applicant, and you can get three different rates depending on which tier you land in.

| Loan Quantum | Tier | Rate Advantage vs Standard |

|---|---|---|

| < S$500K | Standard | baseline |

| S$500K – S$800K | Preferred | ~0.05%–0.10% p.a. sharper |

| S$800K – S$1.5M | Priority | ~0.10%–0.20% p.a. sharper + cashback |

| S$1.5M – S$3M | Jumbo | ~0.15%–0.25% p.a. sharper + legal fee subsidy |

| > S$3M | Private Banking-grade | ~0.20%–0.30% p.a. sharper + relationship perks |

On a S$1.5M loan over 25 years, a 0.20% p.a. rate gap is roughly S$150 per month, or S$45,000 over the full life of the loan. Most new launch buyers sit in the Priority or Jumbo band without realising it. Their relationship banker quotes the standard package, simply because that’s the desk they work at.

SORA Spreads on a Partially-Drawn BUC Loan

Singapore BUC packages are SORA-linked and floating. There is no fixed-rate option during construction; fixed packages are for completed properties. Each tranche draws at the live 3M Compounded SORA plus a bank spread that’s fixed at signing. Spreads run roughly 0.20%–0.75% p.a. depending on your quantum tier. The larger the loan, the tighter the spread.

Your outstanding balance climbs over the build (it sits closer to 50% of the full quantum for the first 18 months or so), so the actual interest you pay in the early years is smaller than on a fully-drawn loan. A 0.20% spread gap on a S$1.5M facility is 0.20% on the average drawn balance, not on the full quantum.

The variable that really matters is how your lock-in lines up with TOP. A 2-year lock-in on a 4-year build reverts to board rate well before TOP, right as the largest tranches disburse. Pick a lender whose lock-in expires shortly after TOP and you keep the option to refinance straight into a sharper post-TOP package.

TOP, Lock-In, and the Refinance Window

Temporary Occupation Permit (TOP) marks the unit habitable and triggers the next 5% disbursement. Most BUC lock-ins run 2–3 years from first disbursement, not from TOP. So depending on how fast the project is built, your lock-in can expire before, at, or after TOP.

| Construction Length | 2-yr Lock-In | 3-yr Lock-In |

|---|---|---|

| 3 years to TOP | Expires 1 year before TOP | Expires at TOP |

| 4 years to TOP | Expires 2 years before TOP | Expires 1 year before TOP |

| 5 years to TOP | Expires 3 years before TOP | Expires 2 years before TOP |

Once it expires, the package reverts to board rate, typically 3.50%–4.50%+ p.a. That’s roughly double the live SORA-linked market. On a S$1.5M loan with three disbursement years left, that works out to S$1,000+ a month in interest you didn’t need to pay.

“The costliest stretch of a Singapore new-launch loan is the period between lock-in expiry and TOP, when you’re stuck on a board rate. Repricing or refinancing inside that window saves more than almost anything else you do in the whole purchase.”

Run the refinance savings calculator 3–4 months before your lock-in expires to see the gap for yourself.

Five Expensive New-Launch Mistakes

- Booking without an IPA. One bank’s pre-approval isn’t enough, because valuations differ and your booking fee evaporates if the loan can’t complete.

- Taking the relationship banker’s quote at face value. A bank officer can only sell their own bank, and will often quote standard pricing when your loan qualifies for a Priority, Jumbo, or Private Banking-grade tier elsewhere.

- A lock-in that expires before TOP. It forces you onto a board rate during the costliest disbursement window. Aim for expiry shortly after TOP instead.

- Chasing the headline spread and nothing else. Your construction timeline, lock-in alignment, and post-TOP refinance plan move far more money than a 0.05% spread today.

- Ignoring second-purchase ABSD. A loan optimised for today’s rate can quietly block a future decoupling or upgrade. Plan for it before the IPA, not after.

How a Nexus Broker Structures the Deal

Nexus is paid by the bank on disbursement, so the service is free to you. The work runs against the OTP and S&P clock:

- Pre-OTP, we have a 30-minute call to map your quantum, tenure, future-purchase plans, CPF, and TDSR/MSR headroom, and to pin down your loan tier.

- On day 1 to 2, we run through the document checklist (payslips, CPF, NOAs, NRIC, existing loans) and submit parallel IPAs to 3–5 lenders matched to your tier.

- On day 3 to 5, the indicative offers come back in writing. We lay them side by side: spread, lock-in against estimated TOP, legal subsidy, cashback, prepayment, and sale clause.

- At OTP signing, your chosen lender’s IPA is already in hand. We coordinate the Letter of Offer, valuation, conveyancing, CPF, and tranche disbursement all the way through to TOP.

- Post-TOP, about 4 months before your lock-in expires, we refresh the market and place the refinance file with the right lender.

Frequently Asked Questions

PPS is the default payment structure for residential Building Under Construction (BUC) projects in Singapore. The buyer pays the developer in instalments tied to construction milestones — 5% booking, 15% on S&P, 10% on foundation, 30% on reinforced concrete framework, 30% on brick walls, ceilings and roof, and the final 10% on TOP and CSC. The bank disburses the loan in matching tranches, so monthly interest is charged only on amounts already drawn, not the full loan.

Yes. New launch booking fees are typically 5% of the purchase price, with a 3-week deadline to sign the Sale and Purchase Agreement. Without a written In-Principle Approval at your exact loan quantum, the booking fee is exposed to TDSR/MSR shortfalls, valuation surprises, and stress test failures. An IPA confirms lending appetite before you commit cash.

Singapore BUC packages are SORA-linked, not fixed. Each tranche is charged at the live 3M Compounded SORA plus a bank spread of roughly 0.20%–0.75% p.a., depending on loan tier. Spread is locked at signing; the SORA component floats. Because outstanding balance ramps as construction progresses, the absolute interest cost in early years is smaller than on a fully-drawn loan.

Yes. New launch loans above S$1.5M typically qualify for jumbo or priority pricing tiers — typically 0.10%–0.25% p.a. sharper than standard, plus legal fee subsidies and cash rebates. Loans above S$3M often access private-banking-grade rates. The catch is that not every bank price-leads at every quantum, which is why parallel IPAs across multiple lenders matter on a large new launch loan.

Most BUC packages have lock-ins extending 1–2 years beyond TOP. Once the lock-in expires, the package reverts to a board rate of 3.50%–4.50%+ p.a., far above market. Start comparing packages 3–4 months before lock-in expiry. Repricing or refinancing then is the highest-value mortgage action a Singapore homeowner can take — typically saving S$1,000–S$1,400 per month on a S$1.5M loan.

Your New Launch Mortgage Broker

Talk to Dan Ler — Nexus Mortgage SG

Independent, paid by the bank on disbursement. I run parallel IPAs across 16+ Singapore lenders, match your file to the right loan-tier rate band, align your lock-in to TOP, and structure the package with your second-property plan already in view.

WhatsApp Dan — New Launch IPA & Rate Review →Run the numbers first: TDSR/MSR affordability calculator to confirm your quantum before submission.

Or get the Free Personalised Mortgage Report — tier-matched comparison from 16 Singapore banks, sent to your inbox in 60 seconds.

Further Reading

- IPA & Independent Mortgage Broker Singapore

- Best Home Loan Rates Singapore 2026

- TDSR & MSR Explained

- MAS 4% Stress Test

- Decoupling Private Property Singapore

- When to Refinance

- MAS: TDSR for Property Loans

- URA: Buying from a Developer

About the author — Dan Ler has advised on Singapore home loans since 2017 at Nexus Mortgage SG, an independent brokerage comparing 16+ MAS-regulated lenders. Nexus is paid by the bank on disbursement, so there is no cost to the borrower.

Nexus Mortgage SG is an independent Singapore mortgage brokerage. This article is general information, not financial advice. Indicative rates and tier bands reflect May 2026 market conditions and are subject to change without notice. Final rates depend on lender, applicant profile, property valuation, and current promotion. PPS milestone percentages follow URA convention; specific projects may vary by minor amounts. MAS regulations and bank lending guidelines are subject to change. Verify current rules at MAS: TDSR for Property Loans before transacting.