How to Buy HDB in Singapore: Your Complete 2026 Step-by-Step Guide

Buying your first HDB flat runs through five stages: the HFE Letter, choosing BTO or resale, picking your loan, the OTP, then completion. This 2026 guide walks you through the mortgage, CPF, and grant decisions you hit at each one.

HDB Eligibility in 2026: Who Can Buy

Start with eligibility. If you fail even one criterion, the loan and the grants are off the table, so it pays to check first. The rules below are for first-time buyers in 2026.

| Requirement | Condition |

|---|---|

| Citizenship | At least one Singapore Citizen in the application |

| Age | At least 21 (35+ for singles under SSC Scheme) |

| Family nucleus | Married couple, fiancé/fiancée, parent-child, orphaned siblings, or singles 35+ |

| Income ceiling (BTO) | S$14,000/month for couples and families (S$21,000 extended); no ceiling on resale |

| Property ownership | Must not own private residential property locally or overseas at application |

| Cooling period | 30-month wait if you sold a previous HDB; MOP rules apply |

| First-timer status | Not previously bought from HDB or taken a CPF housing grant |

Singles aged 35 and above can buy a 2-room Flexi BTO flat in non-mature estates, or any resale flat. Two unmarried Singapore Citizens aged 35 and up can also apply together under the Joint Singles Scheme. The full conditions are on the HDB Buying a Flat portal.

The rules differ for PRs buying an HDB flat, who can only buy resale (never BTO) and face their own scheme, wait-period and financing conditions.

Affordability Checks Before You Shop

Three numbers decide what you can actually buy. Work them out before you set foot in a showflat or book a viewing.

You can run all three through our TDSR/MSR affordability calculator. For the background, read TDSR explained and the MAS 4% stress test. The framework itself is set by MAS.

One thing buyers often miss: the 4% stress test only applies to bank loans. HDB loans are assessed at the headline 2.6% p.a. instead. And the MSR 30% cap is specific to HDB flats and ECs.

The 5-Step HDB Buying Process

The five stages from HFE Letter to keys. The mortgage decision lands at Step 3, but it shapes your eligibility from Step 1 onwards.

Apply for the HFE Letter Mortgage CPF

You need the HFE Letter in hand before you can ballot for a BTO or put in a resale application. It confirms your buyer status, the CPF grants you qualify for, and your maximum HDB concessionary loan. Processing takes 1 to 3 weeks, and the letter stays valid for 9 months. Start here, not at a showflat.

Choose Between BTO and Resale

BTO flats are subsidised and balloted. Resale flats trade on the open market. Here is how the two stack up:

| Factor | BTO | Resale |

|---|---|---|

| Price | Subsidised, below market | Market rate |

| Wait time | 3–5 years (ballot to keys) | 8–14 weeks (OTP to keys) |

| Location | Mostly non-mature estates | Any estate, any block |

| Income ceiling | S$14,000/month for couples; S$21,000 for extended families | No ceiling on purchase |

| CPF grants | EHG up to S$120,000 | EHG + CHG + PHG up to S$230,000 |

BTO works if you can wait and want the biggest subsidy. Resale works if you need to move soon, have your heart set on a particular estate, or earn above the BTO ceiling.

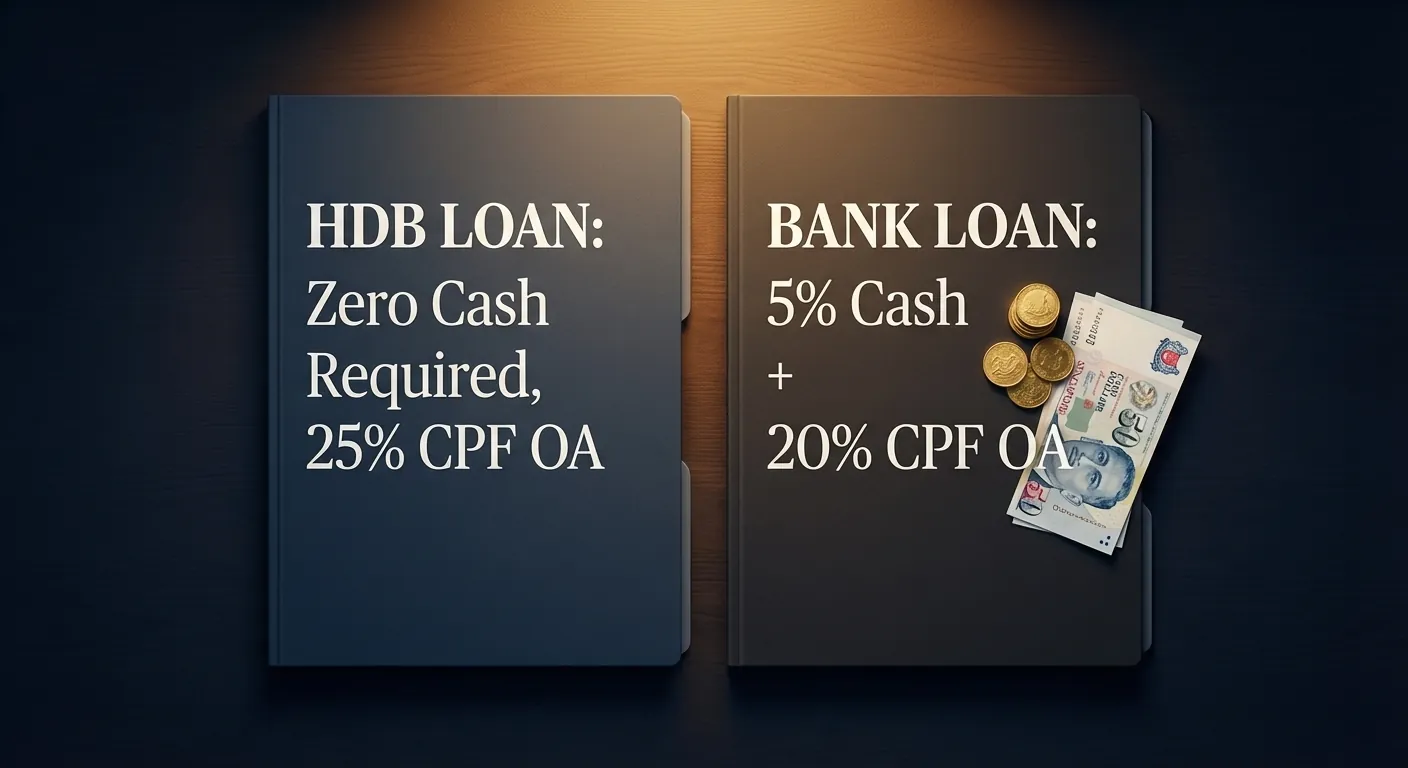

Pick HDB Loan or Bank Loan Critical

This one choice shapes your cashflow for the next 25 years. The HDB concessionary loan sits at 2.6% p.a. (CPF OA + 0.10%), lends up to 75% LTV (cut from 80% on 20 Aug 2024 to match the bank loan cap), and needs no cash at all. Bank loans start from 1.40% p.a. fixed in 2026, also cap LTV at 75%, but require a minimum 5% cash component. We lay it all out in our HDB loan vs bank loan guide. If you are going the bank route, pull an In-Principle Approval (IPA) from each shortlisted lender. It is free, non-binding, and valid for 30 days.

Exercise the Option to Purchase

For a resale flat, you pay an Option Fee of up to S$1,000, then exercise the option within 21 calendar days by paying the Option Exercise Fee. The combined deposit at exercise comes to 5% to 10% of the price and counts towards your downpayment. For a BTO, HDB invites you to a flat selection appointment once your ballot succeeds, and you pay the booking fee on the spot. Either way you will need a conveyancing lawyer, so budget S$2,500 to S$3,500 for that.

Complete the Purchase and Collect Keys CPF

For a resale flat, HDB schedules a completion appointment roughly 8 to 12 weeks after you exercise the OTP. At the appointment you sign the mortgage, execute the CPF charge, settle the balance downpayment plus stamp duty, and collect the keys. A bank loan disburses the same day. An HDB loan disburses directly through HDB. This is where your bank lock-in starts, and where your CPF OA begins covering the monthly instalments. For the full walkthrough across both the HDB and bank routes, see how to apply for a home loan.

CPF Housing Grants Worth Claiming

CPF housing grants do not have to be repaid, and they go straight towards your purchase price or your outstanding loan. First-time buyers often qualify for two or three at once. Your HFE Letter spells out which ones you are eligible for.

Stacked to the maximum, that is S$230,000 on a resale flat (EHG + CHG + PHG) or S$120,000 on a BTO (EHG only). Singles receive half the family rate. The conditions are on the HDB CPF Housing Grants page, and there is more in our guide on using CPF OA for property.

Downpayment: HDB Loan vs Bank Loan

HDB loan and bank loan both cap at 75% LTV (since 20 Aug 2024), so it is a 25% downpayment either way. The difference is the split. The HDB loan can be 100% CPF OA with zero cash, while the bank loan needs a minimum 5% cash and the remaining 20% from CPF OA. On a S$900,000 flat that works out to S$45,000 cash for the bank loan versus zero for the HDB loan.

On a S$900,000 resale flat, the downpayment maths breaks down like this:

| Component | HDB Loan | Bank Loan |

|---|---|---|

| Loan-to-Value (LTV) | Up to 75% | Up to 75% |

| Downpayment required | 25% of purchase price | 25% of purchase price |

| Minimum cash | S$0 — zero cash required | 5% of purchase price |

| CPF OA component | Up to 100% of downpayment | Up to 20% of purchase price |

| On S$900,000 flat: cash | S$0 | S$45,000 minimum |

| On S$900,000 flat: CPF OA | S$225,000 | S$180,000 |

| Interest rate (April 2026) | 2.6% p.a. (CPF OA + 0.10%) | From 1.40% p.a. fixed; typical 1.45%–1.65% — see current home loan rates |

| Stress test | Headline 2.6% | 4.0% MAS floor |

If your savings are thin, the zero-cash downpayment is what makes the HDB loan attractive. The bank loan wins on rate: 1.45% versus 2.6% on a S$720,000 loan saves you roughly S$8,300 in year-one interest. The trade-off is that you have to stay on top of the rate. Fixed and SORA packages reset once the lock-in ends, so you need to refinance when the lock-in expires. And if you need to free up cash down the line, you can tap an equity / cash-out loan.

Common First-Timer Pitfalls

The most common one is skipping the HFE Letter. Buyers go shopping first, then find out their loan ceiling is lower than they assumed. Apply early and let the HFE set your budget.

Another is underbudgeting the side costs. Plan for Buyer’s Stamp Duty, legal fees (S$2,500 to S$3,500), resale agent commission (around 1% + GST), valuation, fire insurance, and renovation. For most resale buyers, a cash buffer of S$50,000 to S$80,000 on top of the downpayment is realistic.

And do not take the first bank quote you are handed. Rates on identical packages can differ by 30 to 50 basis points from one lender to the next, and the legal subsidies and cash rebates vary on top of that. I tell clients to put the quotes side by side before they sign anything.

First-Time Buyer FAQ

Can singles buy an HDB flat in Singapore?

Singles aged 35+ can buy a 2-room Flexi BTO in non-mature estates (SSC Scheme) or any resale flat. Two unmarried Singapore Citizens aged 35+ can apply jointly under the Joint Singles Scheme. EHG for singles is half the family rate.

What is the HDB income ceiling for first-time buyers in 2026?

BTO: household income at or below S$14,000/month for couples and families (S$21,000 for extended families). Resale has no purchase ceiling, but EHG requires household income at or below S$9,000/month for the maximum grant.

How long does the HDB buying process take?

Resale: 8 to 14 weeks from OTP exercise to keys, plus 1 to 3 weeks for the HFE Letter. BTO: 3 to 5 years from successful ballot to keys, depending on construction stage.

Can I use CPF OA for the full HDB downpayment?

Yes — if you take an HDB concessionary loan. The 25% downpayment can be paid entirely from CPF OA with zero cash required. With a bank loan, the 25% downpayment needs a minimum 5% cash; the remaining 20% can come from CPF OA. On a S$900,000 flat: at least S$45,000 cash for a bank loan versus S$0 for an HDB loan. See using CPF OA for property.

What CPF housing grants are available in 2026?

EHG: up to S$120,000 for couples earning S$9,000/month or less (BTO and resale).

CPF Housing Grant: up to S$80,000 for resale buyers with income up to S$14,000/month.

PHG: up to S$30,000 for living with parents (S$20,000 if within 4 km). Resale only.

Maximum stacked on resale for a first-timer couple: S$230,000.

HDB loan or bank loan — which is better?

The HDB loan’s edges: zero cash downpayment (full 25% can be CPF OA), 75% LTV (same as bank loan since 20 Aug 2024), and the option to switch to a bank loan later (the reverse is not allowed). Bank loans offer lower rates — from 1.40% p.a. fixed in 2026 versus 2.6% — but need 5% cash and active refinancing after the lock-in. Full breakdown: HDB loan vs bank loan. For a side-by-side downpayment and CPF cashflow comparison, see the Singapore Mortgage Free Report.

Do I need a mortgage broker to buy an HDB flat?

Not required, but an independent broker compares IPAs across 16+ lenders, weighs rate and rebate together, and stress-tests TDSR/MSR before you commit. Brokers are paid by the bank on disbursement — no cost to the borrower.

About the author — Dan Ler has advised on Singapore home loans since 2017 at Nexus Mortgage SG, an independent brokerage comparing 16+ MAS-regulated lenders. Nexus is paid by the bank on disbursement, so there is no cost to the borrower.

Your Mortgage Broker

Talk to Dan Ler — Nexus Mortgage SG

I check your TDSR, MSR, and CPF position, compare HDB and bank loan packages across 16+ lenders, and guide you through each stage. The bank pays my fee, not you.

WhatsApp Dan Now — Free Consultation →Prefer to run numbers first? Use the affordability calculator with 2026 stress-test logic.

Want every step in one place? Download the Singapore Mortgage Free Report — HFE letter checklist, BTO vs resale timelines and HDB-vs-bank-loan worksheet.

Further reading

- HDB loan vs bank loan — the LTV, tenure and rate trade-offs between the two

- How much CPF OA you can use for housing — Valuation Limit, the 120% Withdrawal Limit and the BRS set-aside after 55

- HDB resale market and your mortgage — how resale pricing feeds into valuation and cash-over-valuation

- How to apply for a home loan — documents, IPA and the order the steps actually happen in

- Affordability check — what you can borrow at the MAS stress floor

General information only, not financial or legal advice. HDB eligibility, grant amounts, and bank rates change. Figures reflect conditions as of April 2026. Official sources: HDB Buying a Flat, CPF home ownership, MAS TDSR.