Best Home Loan for Condo & Private Property in Singapore (2026)

Buying a condo or landed home in Singapore is a different exercise from an HDB purchase. Loans are larger. There is no MSR. And for upgraders, the ABSD clock is ticking. Pick the wrong package and you can lose tens of thousands.

This guide covers what actually matters in 2026: the rates on offer, the rules that cap your loan, the cash you need at completion, and the mistakes that cost private buyers the most.

Private Property Loan Rules in 2026

Before rate-shopping, know the MAS rules that set your hard ceiling. These rules are why condo buyers borrow more than HDB buyers on the same income.

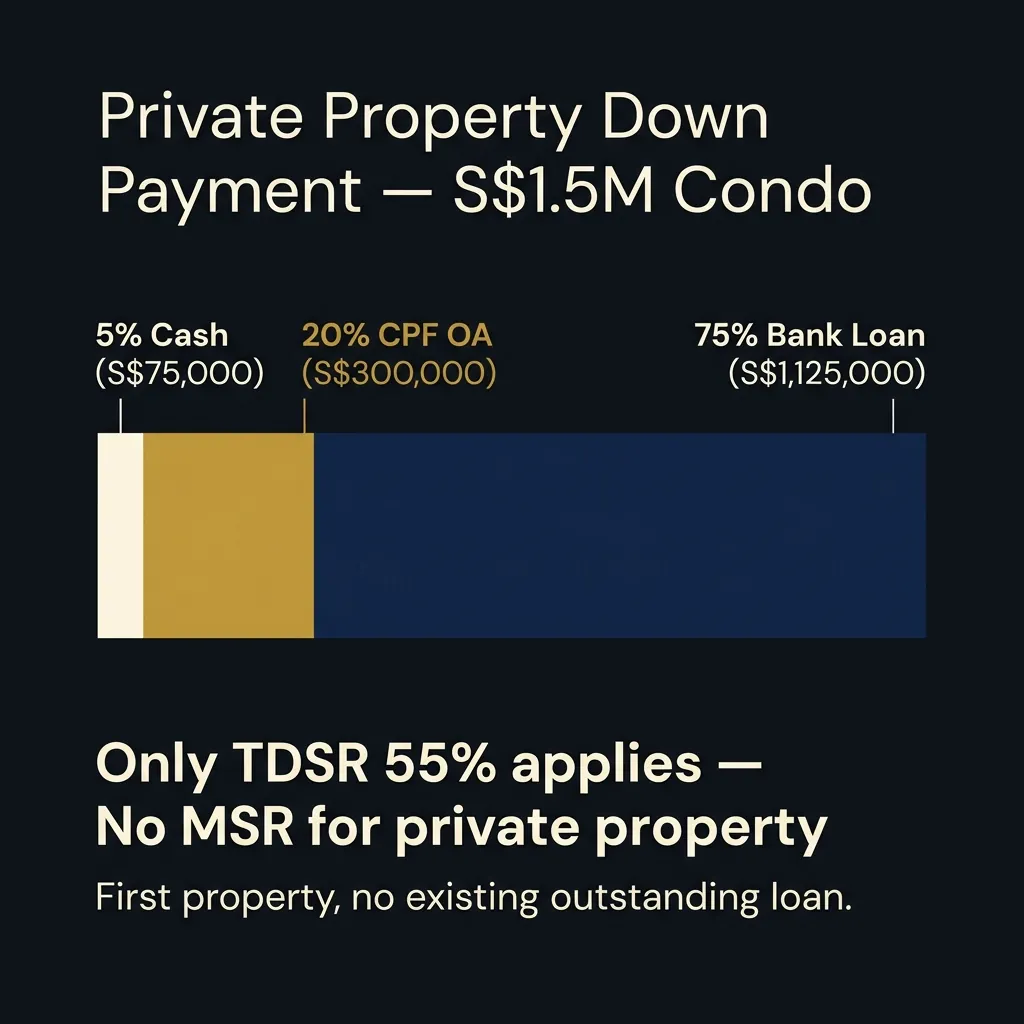

The headline advantage for private buyers: MSR does not apply. HDB buyers face a 30% MSR cap on top of TDSR. For condo and landed, only the 55% TDSR applies — much more borrowing power at the same income.

On a S$1,000,000 loan, the gap between a 1.40% fixed and a 1.65% SORA-linked rate is roughly S$150/month. The gap between a lapsed board rate (4%+) and a repriced one is S$1,500+/month. Discipline at lock-in expiry matters more than the package you start with.

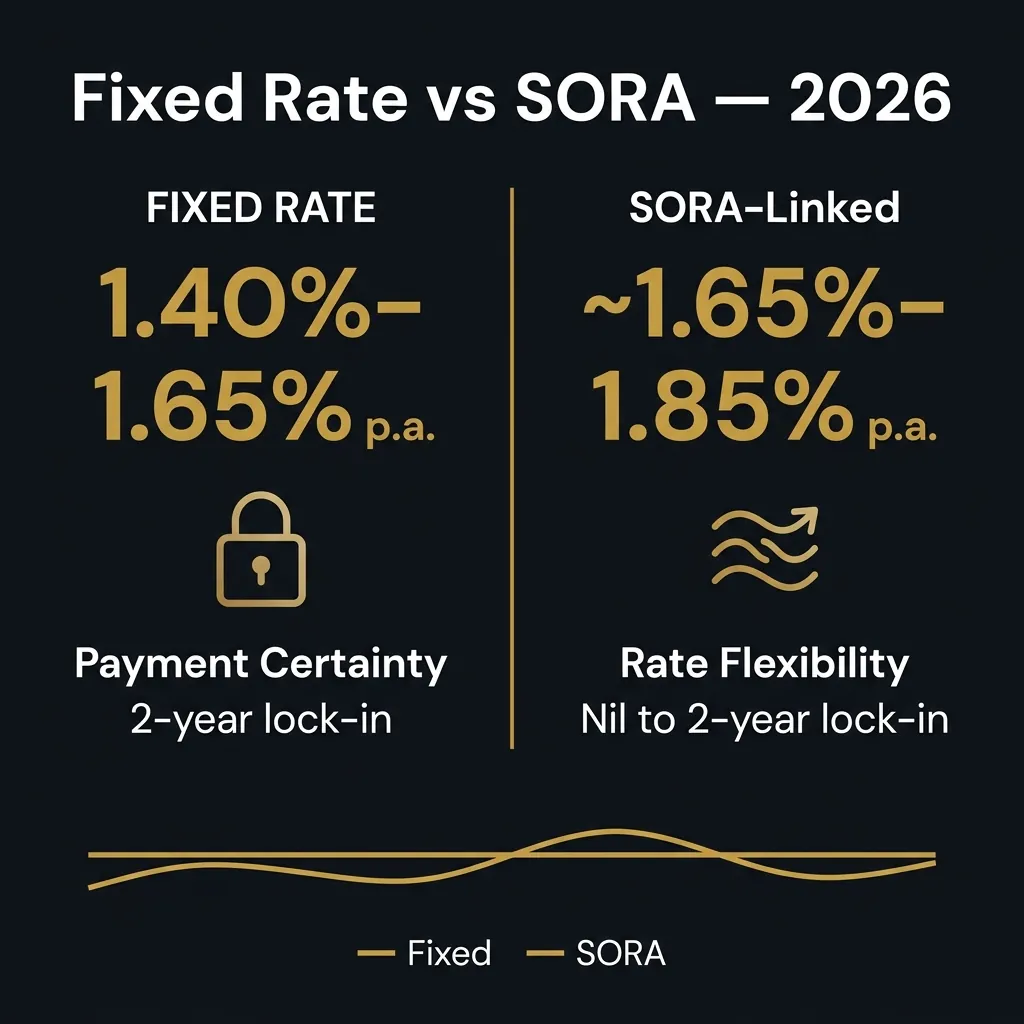

Fixed Rate vs SORA: Which Condo Loan Wins in 2026

Singapore home loans split into two camps: fixed packages (2–3 year lock-ins) and SORA-pegged floating packages. Here is how they compare in April 2026.

| Feature | Fixed Rate | SORA-pegged |

|---|---|---|

| Rate certainty | HIGH | VARIABLE |

| Typical 2026 rate | 1.40%–1.65% p.a. | 1.65%–1.85% p.a. |

| Lock-in period | 2–3 years | 1–2 years (some nil) |

| Early repayment penalty | ~1.5% of outstanding loan | Lower or nil |

| Best when | Rates are high / rising | Rates are falling |

| Monthly payment | Predictable | Can change monthly |

What the rates look like today

Fixed packages start from 1.40% p.a. on jumbo loans (≥ S$1.5M, 5-year lock-in), with typical 2-year fixed in the 1.45%–1.65% range. SORA-linked packages run at 1.55%–1.77% p.a. — based on 3M Compounded SORA at 1.0201% plus a bank spread of 0.20%–0.75%. Jumbo borrowers often get the tightest spreads, which is why high-loan-quantum buyers sometimes find SORA + 0.20%–0.25% the cheapest deal on the market. See the live comparison of current rates across 16+ banks.

The decision is no longer cost. It is certainty vs flexibility. A 2-year fixed gives stable payments for the settling-in period. A SORA package suits buyers who expect rates to drop or want a nil lock-in. Read more on fixed vs SORA.

One rule applies either way: never let the loan revert to the bank's board rate (3.50%–4.50%+) at lock-in expiry. Reprice or refinance every two to three years. Our guide on when to refinance covers the timing.

Fixed (1.40%–1.65% p.a.) and SORA-linked (1.65%–1.85% p.a.) sit unusually close in 2026. Pick on certainty vs flexibility, not cost alone.

— Dan Ler, Nexus Mortgage

Downpayment and CPF Rules for Condo Buyers

Cash demands on a private purchase are bigger than HDB. Know the split before you sign the OTP.

First private property (no existing home loan)

- 25% down (LTV 75%)

- Minimum 5% in cash — CPF cannot cover this

- Up to 20% from CPF OA

- Only TDSR (55%) applies

Second property (HDB or condo still on a loan)

- 55% down (LTV 45%)

- Minimum 25% in cash

- Up to 30% from CPF OA

- 20% ABSD for SC second property (remission if first is sold within 6 months)

Cash table — S$1.5M condo

| Scenario | Min Cash | CPF OA | Bank Loan |

|---|---|---|---|

| First purchase | S$75,000 (5%) | S$300,000 (20%) | S$1,125,000 (75%) |

| Second property | S$375,000 (25%) | S$450,000 (30%) | S$675,000 (45%) |

First-purchase split for a S$1.5M condo: S$75,000 cash + up to S$300,000 CPF OA + S$1.125M bank loan.

BUC (Building Under Construction) loans add a wrinkle: the bank disburses progressively as the developer hits each construction stage, and you only pay interest on the drawn amount. Helpful for cash flow, but factor in that your full instalment kicks in around TOP. Use the TDSR/MSR affordability calculator to stress-test your numbers.

TDSR 55% — The Only Ratio Private Buyers Face

TDSR caps your total monthly debt obligations (home loan + car loan + credit card minimums + other loans) at 55% of gross monthly income. Banks calculate at the MAS 4% stress test floor, not your actual rate. There is no MSR for private property — full breakdown in our TDSR for private property guide.

Worked example. Combined household income S$20,000/month → TDSR ceiling = S$11,000/month. A S$1,500/month car loan leaves S$9,500/month for the home loan. At 4% stress over 30 years, that supports roughly S$1.98M of loan.

The same household buying HDB hits the 30% MSR first — capped at S$6,000/month, supporting only ~S$1.25M. Private buyers get S$730,000 more borrowing capacity at the same income.

Multiply gross monthly household income by 0.55. Subtract every existing monthly debt. The remainder is your maximum instalment. At 4% stress over 30 years, every S$1,000/month supports ~S$209,000 of loan.

How to Secure Your Private Property Loan

-

Stress-test your TDSR with all existing debts

Plug in gross income, car loan, credit cards, and any personal loans. The number sets your property budget — not what a developer brochure quotes.

-

Get an In-Principle Approval (IPA)

Apply to 2–3 banks (or let a broker do it in parallel). Approval takes 1–3 business days. The IPA is valid for 30 days and signals seriousness when you submit an OTP.

-

Compare the full package, not just the headline rate

Effective rate over the lock-in, lock-in length, prepayment penalty, repricing terms, and legal fee subsidies. A broker models all 16+ banks side-by-side.

-

Exercise the OTP within 21 days

Pay BSD (1%/2%/3%/4%/5%/6% tiered) and any ABSD within 14 days of exercise. The bank's valuation and Letter of Offer must land in this window.

-

Appoint a panel solicitor

Bank panel firms unlock legal subsidies (S$1,800–S$2,500). The solicitor handles title search, CPF charge, and completion.

-

Disbursement and completion

The bank disburses to the seller via your solicitor. You get the keys. The mortgage is registered with the Singapore Land Authority.

How 16 Banks Compare for Condo Loans in 2026

Rates move weekly; structural differences between lenders are stable. The split below has held for the past two years.

| Lender type | Rate competitiveness | Legal subsidy | Approval speed | Best for |

|---|---|---|---|---|

| DBS / POSB | HIGH | YES | FAST | DBS payroll customers |

| OCBC | HIGH | YES | MEDIUM | HDB + private loans |

| UOB | HIGH | YES | MEDIUM | Flexible repricing |

| SCB / Citibank | MID | YES | MEDIUM | Foreign / PR buyers |

| HSBC | MID | YES | MEDIUM | High-income professionals |

| Maybank / RHB | MID | VARIES | FAST | Malaysian PR buyers |

The top three local banks (DBS, OCBC, UOB) usually sit within 0.05%–0.10% of each other. On a S$500,000 loan over two years that's S$500–S$1,000. Legal subsidies, cashback, and free repricing windows can outweigh a small rate gap. See the Association of Banks in Singapore for the full lender list.

When banks see a competing submission via a broker, concessions of 0.05%–0.10% appear that walk-in customers miss. On a S$600,000 loan over 25 years, 0.10% is roughly S$15,000 in interest.

5 Mistakes Condo Buyers Keep Making

Five avoidable mistakes that cost private buyers tens of thousands.

1. Underestimating ABSD on a second property

ABSD is the largest upfront cost after the unit itself, and it depends on residency and property count.

| Buyer Profile | 1st | 2nd | 3rd+ |

|---|---|---|---|

| Singapore Citizen | 0% | 20% | 30% |

| Singapore PR | 5% | 30% | 35% |

| Foreigner (non-FTA) | 60% | 60% | 60% |

| FTA nationals* | 0% | 20% | 30% |

| Entity | 65% | 65% | 65% |

*US, Swiss, Liechtenstein, Icelandic, Norwegian. Source: IRAS ABSD.

On a S$1.5M condo: SC second property = S$300,000 ABSD; PR = S$450,000; foreigner = S$900,000. Citizens can claim remission only if the first home is sold within 6 months of completion (new launch) or OTP exercise (resale). For couples, a decoupling case study can be cheaper than paying ABSD — but only after running the BSD math.

2. Not stress-testing TDSR with existing car loans and credit cards

An S$80,000 car loan can wipe out S$300,000 of borrowing capacity at the 4% stress floor. Run the TDSR before you sign the OTP, not after the bank rejects the loan amount you assumed.

3. Forgetting the LTV drop on a second loan

Buying private while still on an HDB loan drops LTV from 75% to 45%. On a S$1.5M condo, that's S$825,000 out of pocket. Sell first, decouple, or arrange bridging — model it before the OTP.

4. Underestimating BSD on jumbo property

BSD is tiered (1%/2%/3%/4%/5%/6%) and bites hardest above S$1.5M. On a S$3M condo, BSD is roughly S$144,600 — payable in cash within 14 days of OTP exercise. Add it to your cash plan early.

5. Drifting onto the board rate at lock-in expiry

Banks default to the board rate (3.50%–4.50%+) once your fixed period ends. On a S$1M loan that's S$1,500+/month of avoidable interest. Diary the lock-in expiry and use the refinance savings calculator three months before. If you have built equity, an equity / cash-out loan may also be worth comparing.

Get your free condo loan comparison

We compare 16+ MAS-regulated banks in one submission and present the best fit — fixed, SORA, BUC, or jumbo. No fees to you.

WhatsApp Dan — Free ComparisonPrefer to read first? Download the Singapore Mortgage Free Report — Dan's full first-time-buyer playbook with TDSR, BSD, ABSD and lock-in worksheets.

Frequently Asked Questions

First private purchase: 25% down (at least 5% cash, up to 20% CPF OA). Second loan: 55% down (at least 25% cash, up to 30% CPF OA).

Fixed packages run from 1.40% p.a. (jumbo, 5-year) with typical 2-year fixed at 1.45%–1.65%. SORA-linked sits at 1.55%–1.77% p.a. (3M SORA 1.0201% + spread of 0.20%–0.75%). Pick fixed for certainty during settling-in. Pick SORA for flexibility or jumbo loans where the spread is tightest. Never let either revert to a board rate at expiry.

No. MSR applies only to HDB and ECs within MOP. For condos and landed homes, only the 55% TDSR applies — private buyers get more borrowing power at the same income.

SC: 20% second / 30% third+. PR: 30% / 35%. Foreigner: flat 60%. FTA nationals (US, Swiss, Liechtenstein, Icelandic, Norwegian): same as SC. Entity: 65%. On a S$1.5M condo, SC second-property ABSD is S$300,000. Citizens get remission if they sell their first home within 6 months. Source: IRAS.

IPA: 1–3 business days. Full approval after valuation: 5–10 business days. The IPA is valid for 30 days — useful for new launches with longer timelines.

No. Nexus is paid by the bank on disbursement. Your rate is the same or better than a walk-in application, with all 16+ lenders compared in one submission.

Further Reading

- Singapore Mortgage Free Report — Dan's full pre-purchase playbook: purchase timeline (variant-driven, HDB or Private), TDSR/MSR at the MAS 4% stress floor, BSD/ABSD upfront-cost breakdown, LTV/IWAA tenure trade-off, lock-in expiry playbook and a 16-bank rate comparison in one downloadable PDF

- How to Apply for a Home Loan in Singapore — the full step-by-step, HFE/IPA to drawdown

- Singapore Home Loan Rates 2026 — Fixed vs SORA

- TDSR for Private Property — How Much Can You Borrow?

- MAS 4% Stress Test Explained

- When to Refinance Your Home Loan

- Decoupling Case Study for Second-Property Buyers

- Using CPF OA for Property

About the author — Dan Ler has advised on Singapore home loans since 2017 at Nexus Mortgage SG, an independent brokerage comparing 16+ MAS-regulated lenders. Nexus is paid by the bank on disbursement, so there is no cost to the borrower.

For general information only; not financial advice. Rates indicative as of April 2026 and subject to change. Refer to MAS TDSR, IRAS ABSD, and IRAS BSD for official rules. Consult a licensed mortgage broker before borrowing.