In-Depth Guides & Analysis

Practical, unbiased breakdowns of Singapore's mortgage regulations and lending landscape.

SIBOR Rate Singapore: The Benchmark No Longer Exists

Searching for the SIBOR rate today? There isn't one. The 6-month tenor ended 31 March 2022 and the 1-month…

Read More

15-Month Wait-Out Period Removed: Private Owners Can Buy HDB Resale Immediately

MND scrapped the 15-month wait-out with immediate effect on 28 July 2026 — private property owners and…

Read More

Thomson Reserve (Former Thomson View): Financing Guide Before the 2026 Preview

Thomson Reserve is the former Thomson View, redeveloped by UOL, SingLand and CapitaLand Development: ~1,268…

Read More

Dunearn House: Pricing & Financing Guide 2026 (Bukit Timah Turf City)

Dunearn House is the first private condo in the new Bukit Timah Turf City — 380 units, 99-year lease, 2BR…

Read More

Caveat Loan Singapore 2026: Fast Property-Secured Business Financing

A caveat loan is a short-term private loan secured by a caveat on property you already own — fast (1–3 days)…

Read More

Singapore Mortgage Rate Outlook 2026: Where SORA & Fixed Rates Sit Now

Where Singapore mortgage rates sit in mid-2026 (3-month SORA near 1.08%), what actually drives them, and what…

Read More

Reprice vs Refinance in Singapore 2026: Which Actually Saves More?

Reprice (stay with your bank) or refinance (switch banks)? The cost, speed and savings compared, when each…

Read More

FDR, FHR & DMR: Singapore's Fixed-Deposit Home Loan Pegs Explained

FHR, FDR, FDMR, FDPR and DMR are bank fixed-deposit home-loan pegs. What each means, how they differ from…

Read More

Foreigner & PR Buying Private Property Singapore 2026: ABSD & Loan Guide

Foreigners pay 60% ABSD on Singapore residential property; PRs pay 5% — and US and EFTA nationals are exempt…

Read More

Fixed vs Floating Home Loan Singapore 2026: Which to Pick

Fixed locks your rate for the lock-in; floating tracks 3-month SORA plus a spread and often allows free…

Read More

Bridging Loan Singapore 2026: How It Works for Upgraders

The short-term loan that covers your next downpayment before your current home is sold. How it works, the…

Read More

Singapore Stamp Duty 2026: BSD + ABSD Calculator & Guide

Buyer's Stamp Duty bands and ABSD rates for Citizens, PRs and foreigners, with a free BSD + ABSD calculator…

Read More

Lentor Gardens Residences 2026: Cheapest Lentor Land & How to Finance It

Kingsford secured the Lentor Gardens site at ~$920 psf ppr — the lowest land cost in the entire Lentor cycle…

Read More

Refinancing Your HDB Loan to a Bank Loan in 2026: Is Leaving the 2.6% Worth It?

HDB charges 2.6% while banks offer ~1.4% in 2026 — the widest gap in years. The real savings by loan size…

Read More

Refinancing a Home Loan in Singapore (2026): A Real Case Study

A real refinance: an early-30s couple moved their $1.2M condo loan from 2.45% to 1.35% fixed, cutting the…

Read More

Upgrading From HDB to Condo in Singapore (2026): A Real Case Study

A real upgrader case: a couple sold their 4-room HDB and bought a $2.09M condo. Selling first meant the condo…

Read More

How to Avoid ABSD on a Second Property in Singapore (Legally): A Real Decoupling Case Study

A real client paid about S$5,000 to decouple a Yishun condo and legally avoided roughly S$163,000 in ABSD on…

Read More

How to Apply for a Home Loan in Singapore (2026): Step-by-Step

The full 2026 application playbook. Work out your budget under TDSR 55% / MSR 30% at the MAS 4% stress floor…

Read More

Commercial Property Loan Singapore 2026: Rates, LTV & Eligibility

Commercial & industrial property loans sit outside the residential rules — no CPF, no ABSD, LTV up to 80–90%…

Read More

Cash-Out Refinance Singapore 2026: Unlock Property Equity

Cash-out refinance (equity term loan) lets you borrow against private-property equity and take the difference…

Read More

Joint Tenancy vs Tenancy-in-Common Singapore 2026: Decoupling, the 99-1 Trap and ABSD Planning

JT = equal undivided + survivorship. TIC = defined shares (up to 99/1) + no survivorship. 99/1 ratio is LEGAL…

Read More

$1 Million HDB Flats Singapore 2026: Worth Buying? Financing & the HDB-vs-EC-vs-Condo Decision

Q1 2026 set a record with 412 HDB resale flats sold at S$1 million or more — up 23.4% YoY, average price…

Read More

CPF Accrued Interest on Property Sale (2026): Why Your Cheque Is Smaller

CPF accrued interest is the 2.5% p.a. monthly-compounded interest your CPF OA would have earned if not…

Read More

Above the HDB Income Ceiling? Buy Resale Anyway — HFE + Bank Loan + IPA Guide (2026)

HDB resale has no income ceiling on the purchase itself. The S$14,000 family / S$21,000 extended / S$7,000…

Read More

SSD Singapore 2026: The 4 July 2025 Reset Explained (16/12/8/4% over 4 Years)

MAS reset Seller's Stamp Duty on 4 July 2025: holding period extended from 3 to 4 years, every tier raised by…

Read More

Singapore PR Buying HDB Flat 2026: Eligibility, ABSD & Loan Guide

Singapore PRs can only buy HDB resale, never BTO. Full 2026 guide to the four HDB schemes open to SPRs…

Read More

Hudson Place Residences (one-north): Indicative Pricing & Financing Guide for May 2026

Hudson Place Residences drew 3,500+ visitors over the May Day weekend. 327 units at one-north, indicative…

Read More

New Launch Condo Financing Singapore (2026): Progressive Payment, IPA & TOP Strategy

A new launch is a S$1.5M–S$5M+ commitment with a three-week S&P clock and a five-year construction tail. The…

Read More

EC MOP Doubled to 10 Years — What May 2026's Executive Condo Reset Means for Your Mortgage

MND just doubled the EC Minimum Occupation Period to 10 years, lifted the first-timer quota to 90% with a…

Read More

IPA & Independent Mortgage Broker Singapore 2026: Why Both Matter Before You OTP

An IPA protects your 1% OTP deposit; an independent broker pulls every Singapore bank in parallel and places…

Read More

Self-Employed TDSR Singapore: How the 30% Haircut Really Works in 2026

MAS forces banks to chop 30% off every dollar of self-employed income before TDSR applies. Full 2026…

Read More

HDB Resale Prices Just Fell for the First Time in 7 Years — What Q1 2026 Means for Your Mortgage

HDB resale prices dipped 0.1% in Q1 2026 — the first decline since 2019. With fixed home loan rates from…

Read More

Decoupling Property in Singapore: A $5M Landed House Case Study

Learn how property decoupling works to save on ABSD. We break down the exact costs, stamp duties, and CPF…

Read More

MAS 4% Stress Test Singapore: 2026 Mortgage Guide

Learn how the MAS 4% stress test caps your borrowing in Singapore. A clear 2026 guide to TDSR, MSR, and how…

Read More

HDB Home Loan vs Bank Loan: Which Is Right for You?

Choosing the right HDB home loan can save you thousands. A definitive 2026 comparison of rates, LTV limits…

Read More

How to Buy HDB in Singapore: 2026 Step-by-Step Guide

From HFE Letter to key collection — a clear step-by-step guide for first-time buyers in Singapore in 2026…

Read More

TDSR Private Property Singapore: What Buyers Must Know

Buying private property in Singapore? TDSR 55% caps your loan — MSR does not apply. Full 2026 breakdown with…

Read More

Best Home Loan for Condo & Private Property in Singapore (2026)

Buying a condo or landed property? Compare fixed vs SORA rates from 16 banks, understand TDSR limits, ABSD…

Read More

CPF Home Loan Singapore: Using Your OA for Property

CPF home loan rules in Singapore explained for 2026 — OA withdrawal limits, the Basic Retirement Sum rule…

Read More

Refinance Home Loan Singapore: When & How to Save in 2026

Refinance your home loan in Singapore at the right time and save up to S$60,000. 2026 guide on lock-in…

Read More

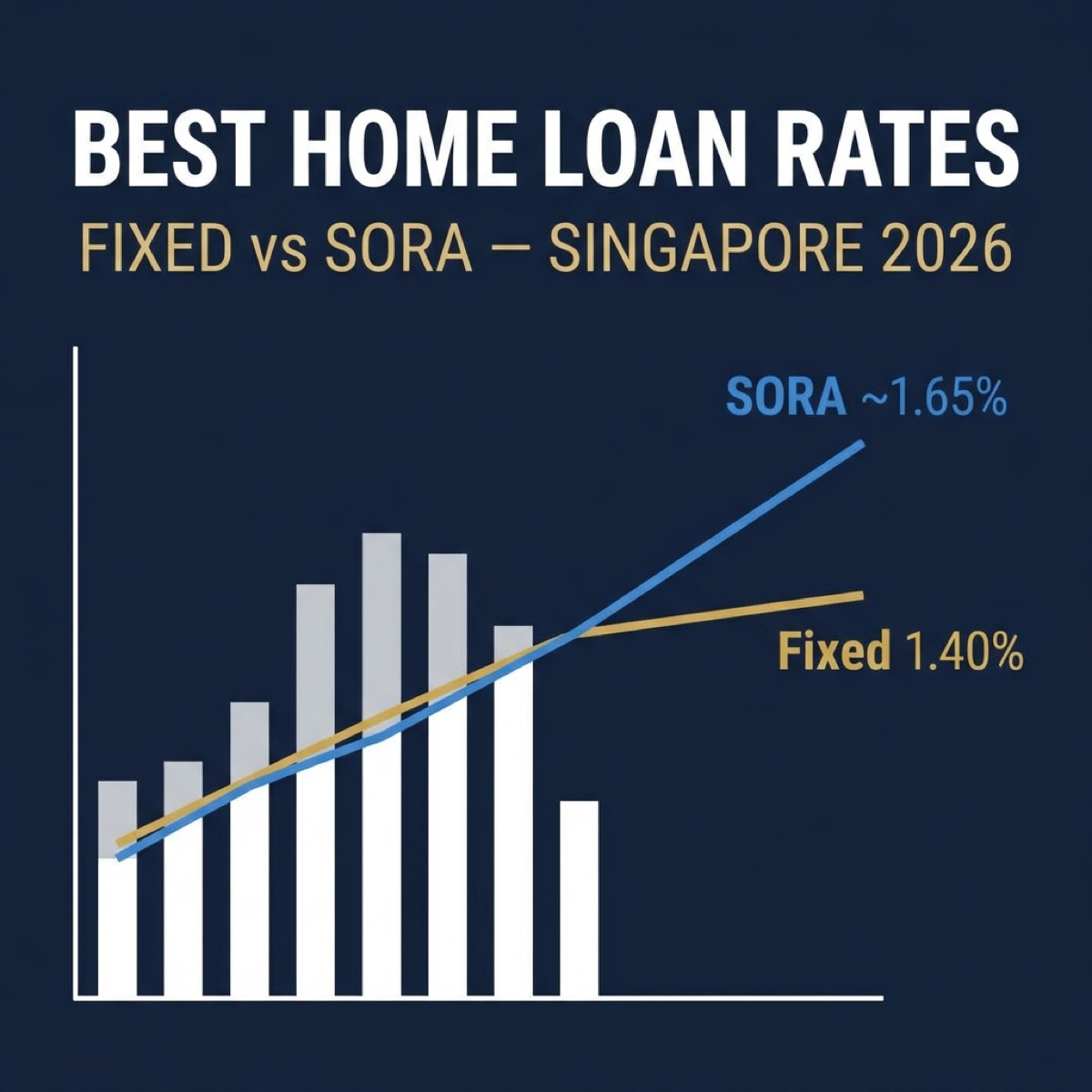

Best Home Loan Rates Singapore 2026: Fixed vs SORA Compared

Fixed rates from 1.40% p.a. vs SORA-linked at ~1.65–1.85% (3M SORA at 1.06%). What the best home loan rates…

Read More

DBS vs UOB vs OCBC Home Loans 2026: Which Bank Fits Your Profile?

Headline rates across the big three sit within basis points of each other — the money is won and lost in…

Coming Soon

Singapore Property Cooling Measures in 2026: Every Rule That Affects Your Purchase

The consolidated map, current to August 2026: ABSD at the April 2023 schedule (SC 20% second, foreigner 60%)…

Coming Soon

MRTA vs HPS vs Term Life: Mortgage Insurance in Singapore, Explained

HPS is mandatory for HDB owners paying with CPF; private-property owners choose between MRTA and level term …

Coming Soon

How an SME Funded a S$11.6M Project With a S$4M Equity Term Loan on Its Industrial Property

Real case study: the company won a S$11.6M project but was S$4M short on equipment funding. It unlocked S$4M…

Coming Soon

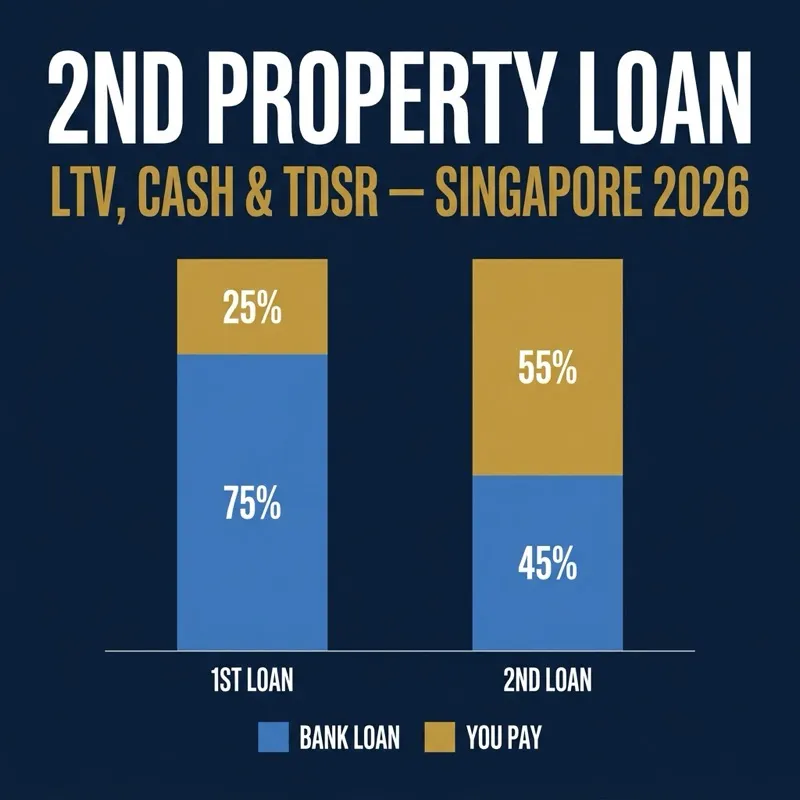

Second Property Loan in Singapore: LTV, Cash and TDSR

A second housing loan is capped at 45% LTV, not 75% — and at least 25% of the price must be hard cash that…

Coming Soon

SME Caveat Loans: How Property-Backed Financing Works

A plain-English guide to SME caveat loans in Singapore — how lenders calculate LTV against existing bank…

Coming SoonFixed vs Floating Home Loan Singapore 2026: Which to Pick

Fixed locks your rate; floating tracks SORA and often allows free conversion. The real differences beyond the rate, when each wins, and a simple way to decide.

Read MoreBridging Loan Singapore 2026: How It Works for Upgraders

The short-term loan that covers your next downpayment before your current home is sold. How it works, the cost on the bridged amount only, the six-month TDSR exemption, and a worked HDB-to-condo example.

Read MoreSingapore Stamp Duty 2026: BSD + ABSD Calculator & Guide

Buyer's Stamp Duty bands and ABSD rates for Citizens, PRs and foreigners, with a free BSD + ABSD calculator, worked examples, and why stamp duty is cash on top of your downpayment.

Read MoreLentor Gardens Residences 2026: Cheapest Lentor Land & How to Finance It

Kingsford secured the Lentor Gardens site at ~$920 psf ppr — the lowest land cost in the entire Lentor cycle, while the next parcel hit a record $1,278. Indicative ~$2,150 psf · 499 units (2BR–4BR). The BUC financing playbook: 75% LTV, TDSR, progressive payments, IPA.

Read MoreUpgrading From HDB to Condo in Singapore (2026): A Real Case Study

A couple sold their 4-room HDB and bought a $2.09M condo. Selling first meant $0 ABSD instead of fronting $418,000 — and a 2-week bridging loan closed the timing gap. The sell-first vs buy-first decision, CPF refund, 75% LTV and TDSR.

Read MoreHow to Avoid ABSD on a Second Property in Singapore (Legally): A Real Decoupling Case Study

A real client paid about S$5,000 to decouple a Yishun condo and legally avoided roughly S$163,000 in ABSD on a second condo — now up S$442,000. The 99-1 structuring move, the step-by-step route, and the IRAS 99-1 line that keeps it legal.

Read MoreHow to Apply for a Home Loan in Singapore (2026): Step-by-Step

The full 2026 application playbook: fix your budget under TDSR 55% at the 4% floor, get an HFE letter or bank IPA before you sign the OTP, compare packages across 16 banks, and complete documents to drawdown.

Read MoreCommercial Property Loan Singapore: Eligibility & How to Qualify (2026)

Commercial and industrial property financing in 2026: rates from ~1.08%, up to 90% LTV, no CPF and no ABSD, company-vs-personal TDSR, GST, and why an independent broker closes the rate gap.

Read MoreHow Cash-Out Refinancing Works in Singapore (2026 Guide)

Turn private-property equity into cash at home-loan rates. The equity term-loan formula, 75%/45% LTV, the CPF deduction that shrinks your release, TDSR limits, and a full worked example.

Read MoreJoint Tenancy vs Tenancy-in-Common Singapore 2026: Decoupling, the 99-1 Trap and ABSD Planning

How the manner of holding decides your decoupling cost: joint tenancy vs tenancy-in-common, ownership ratios, the 99-1 trap and IRAS clawback, and ABSD planning for couples buying again.

Read More$1 Million HDB Flats Singapore 2026: Worth Buying? Financing & the HDB-vs-EC-vs-Condo Decision

412 record million-dollar HDB sales in Q1 2026. The full financing math — MSR/TDSR check, BSD — and the $1M HDB vs $1.4M EC vs $2M condo decision.

Read MoreCPF Accrued Interest on Property Sale (2026): Why Your Cheque Is Smaller

Why your sale proceeds come back smaller than expected: the 2.5% CPF accrued-interest formula, HDB and private worked examples, the opportunity cost, and the pay-down trap when rates dip.

Read MoreAbove the HDB Income Ceiling? Buy Resale Anyway — HFE + Bank Loan + IPA Guide (2026)

Over the S$14,000 HDB income ceiling? You can still buy an HDB resale — just not with the HDB loan. The HFE letter, 75% bank-loan LTV, and why the IPA matters.

Read MoreSSD Singapore 2026: The 4 July 2025 Reset Explained (16/12/8/4% over 4 Years)

The 4 July 2025 Seller's Stamp Duty reset: holding period extended from 3 to 4 years and rates raised 4 points. Private 16/12/8/4% over Y1–Y4, with hold-vs-sell math.

Read MoreSingapore PR Buying HDB Flat 2026: Eligibility, ABSD & Loan Guide

Singapore PRs can buy HDB resale only, never BTO. The PR schemes, the 3-year SPR wait, 5% ABSD, bank-loan-only financing, and the MSR/TDSR and CPF rules.

Read MoreHudson Place Residences (one-north): Indicative Pricing & Financing Guide for May 2026

Hudson Place Residences at one-north: 327 units, indicative pricing, BSD/TDSR math, the BUC progressive-payment timeline, and an IPA + fixed-vs-SORA rate strategy.

Read MoreNew Launch Condo Financing Singapore (2026): Progressive Payment, IPA & TOP Strategy

A new launch is a S$1.5M–S$5M+ commitment with a three-week S&P clock and a five-year construction tail. The IPA, the loan tier, and the fixed-vs-SORA call decide the next 25 years of cashflow.

Read MoreEC MOP Doubled to 10 Years — What May 2026's Executive Condo Reset Means for Your Mortgage

MND just doubled the EC Minimum Occupation Period to 10 years, lifted the first-timer quota to 90% with a 2-year priority window, and scrapped the Deferred Payment Scheme. What Singapore EC buyers and upgraders should do about their mortgage now.

Read MoreHDB Resale Prices Just Fell for the First Time in 7 Years — What Q1 2026 Means for Your Mortgage

HDB resale prices dipped 0.1% in Q1 2026 — the first decline since 2019. With fixed home loan rates from 1.40% and SORA from 0.97%, here's how Singapore buyers, upgraders, and refinancers should position their financing now.

Read MoreIPA & Independent Mortgage Broker Singapore 2026: Why Both Matter Before You OTP

An IPA protects your 1% OTP deposit; an independent broker pulls every Singapore bank in parallel and places your loan in the right rate tier. Why bias-free comparison and exit-planning matter in 2026.

Read MoreSelf-Employed TDSR Singapore: How the 30% Haircut Really Works in 2026

MAS forces banks to chop 30% off every dollar of self-employed income before TDSR applies. Full 2026 breakdown of the haircut math, the 2-year NOA rule, and pledge-fund vs show-fund strategies that recover lost borrowing power.

Read MoreDecoupling Property in Singapore: A $5M Landed House Case Study

Learn how property decoupling works to save on ABSD. We break down the exact costs, stamp duties, and CPF refunds using a realistic $5M landed house example for 2026.

Read MoreMAS 4% Stress Test Singapore: 2026 Mortgage Guide

Learn how the MAS 4% stress test caps your borrowing in Singapore. A clear 2026 guide to TDSR, MSR, and how to calculate your exact home loan eligibility.

Read MoreHDB Home Loan vs Bank Loan: Which Is Right for You?

Choosing the right HDB home loan can save you thousands. A definitive 2026 comparison of rates, LTV limits, CPF rules, and the true cost over a 25-year tenure.

Read MoreHow to Buy HDB in Singapore: 2026 Step-by-Step Guide

From HFE Letter to key collection — a clear step-by-step guide for first-time buyers in Singapore in 2026, covering CPF, loan options, and TDSR at every stage.

Read MoreTDSR Private Property Singapore: What Buyers Must Know

Buying private property in Singapore? TDSR 55% caps your loan — MSR does not apply. Full 2026 breakdown with worked calculation examples and free advice.

Read MoreBest Home Loan for Condo & Private Property in Singapore (2026)

Buying a condo or landed property? Compare fixed vs SORA rates from 16 banks, understand TDSR limits, ABSD rules, and down payment requirements for private property in 2026.

Read MoreCPF Home Loan Singapore: Using Your OA for Property

CPF home loan rules in Singapore explained for 2026 — OA withdrawal limits, the Basic Retirement Sum rule, accrued interest, and what private property buyers must know.

Read MoreRefinance Home Loan Singapore: When & How to Save in 2026

Refinance your home loan in Singapore at the right time and save up to S$60,000. 2026 guide on lock-in timing, SORA vs fixed rates, legal fees, and free advice.

Read MoreBest Home Loan Rates Singapore 2026: Fixed vs SORA Compared

Fixed rates from 1.40% p.a. vs SORA-linked at ~1.65–1.85%. What the best home loan rates in Singapore look like right now, and how to secure one across all 16+ lenders.

Read MoreSME Caveat Loans: How Property-Backed Financing Works

A plain-English guide to SME caveat loans in Singapore — how lenders calculate LTV against existing bank mortgages and CPF charges, and what business owners need to know.

Coming Soon